Terence S. Phillips,

|

Back to Blog

5 Ways To Reduce Income Inequality6/27/2020

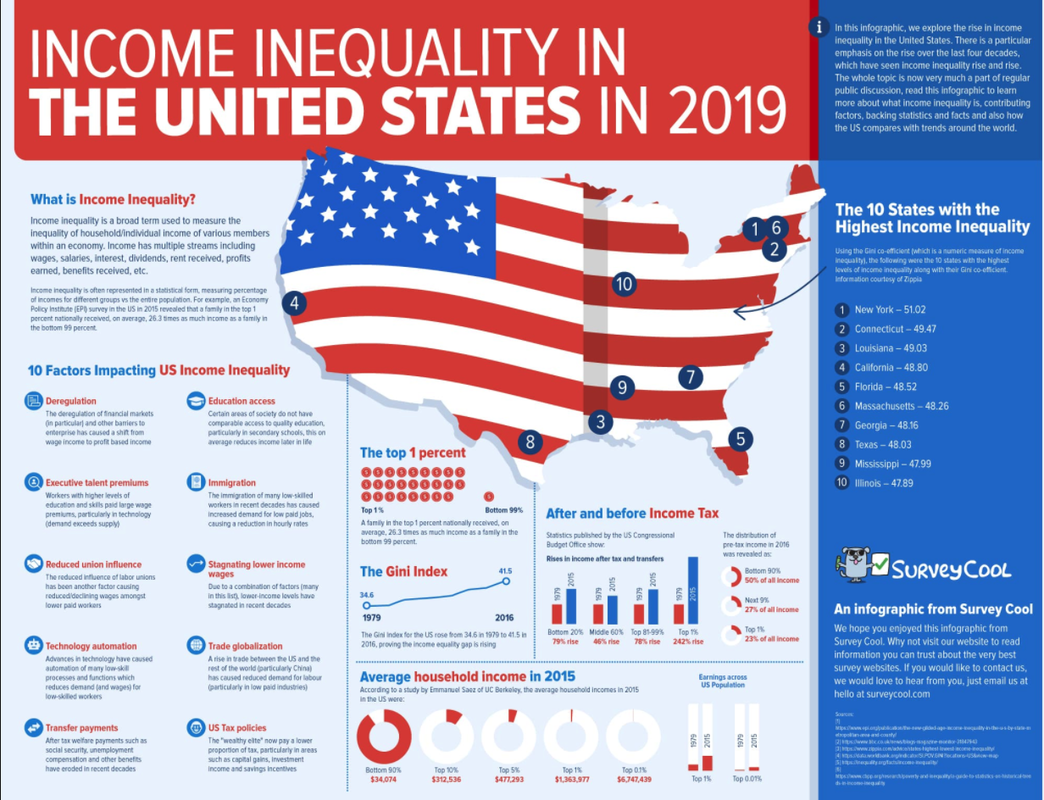

The income inequality gap in the United States is growing. Programs providing better basic education and job training would better prepare workers to compete in the economy. Progressive tax laws could drum up the revenue needed to fund these programs. These are just some of the solutions to ending income inequality in the U.S.

0 Comments

Back to Blog

Visit https://www.consumerfinance.gov/about... to learn more about coronavirus mortgage relief options under the CARES Act.

Visit https://www.consumerfinance.gov/coron... for more information about protecting and managing your finances due to the financial impact of the national coronavirus emergency. If you are experiencing difficulty making on-time mortgage payments due to the national coronavirus emergency, forbearance may be an option for you. Forbearance can help consumers get back on their feet during short-term financial difficulty, but there are a few things you need to know and some important decisions you’ll need to make. Forbearance is when your mortgage servicer, that’s the company that sends your mortgage statement and manages your loan, or lender allows you to pause or reduce your payments for a limited period of time. Forbearance does not erase what you owe. You’ll have to repay any missed or reduced payments in the future. So, if you’re able to keep up with your payments, keep making them. The types of forbearance available vary by loan type. If your mortgage is backed by the federal government—this includes FHA, VA, USDA, Fannie Mae and Freddie Mac loans—provisions of the recently enacted CARES Act allow you to suspend payments for up to twelve months if you are experiencing financial difficulty due to the impact of the coronavirus on your finances. Loan servicers may also have forbearance or deferment options for non-government backed or private loans, but the exact options available to you may differ. Here’s how this works for federally-backed mortgages under the CARES Act. If you are experiencing financial hardship due to the coronavirus pandemic, you have a right to request forbearance for up to one hundred eighty days. You also have the right to request an extension for up to an additional one hundred eighty days. But, you must contact your loan servicer to request this forbearance. There won’t be any additional fees, penalties or interest added to your account. But, your regular interest will still accrue. Other than telling your servicer that you have a pandemic-related financial hardship, you won’t need to submit additional documentation to qualify for this forbearance. It’s important to find out what options are available to you. The best place to find that information is from your loan servicer. Look for their contact info on your monthly mortgage statement. Right now, most financial institutions, including mortgage servicers, are experiencing high call volumes, so there may be long wait times to talk to someone on the phone. Regardless of the type of mortgage you have or how you communicate with your servicer, here are some things to consider. If you cannot make your mortgage payments, and you are looking to suspend or reduce your payments, you will need to work with your servicer. If you decide to move forward with a forbearance plan, ask your servicer how you will be required to pay back the amount owed after the forbearance period. Will you owe the entire unpaid amount in a lump sum once the pause period has ended or at the end of the loan term? Can the loan term be extended so that missed payments are added to the end of your mortgage? Will your subsequent monthly payments be higher for a period of time to make up the deferred amount? Finally, be on the lookout for scams and scammers looking to take advantage of consumers affected by coronavirus. You might receive fraudulent calls, emails, text messages or other “offers” to help you reduce or stop your mortgage payments. Make sure you are working directly with your mortgage servicer.

Back to Blog

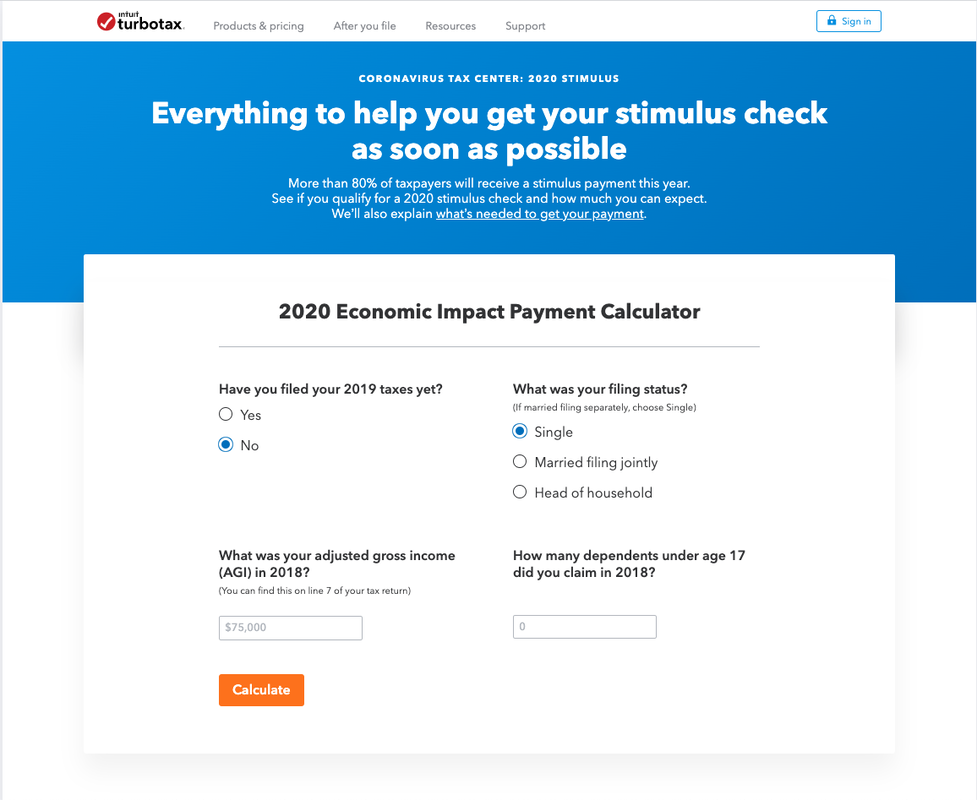

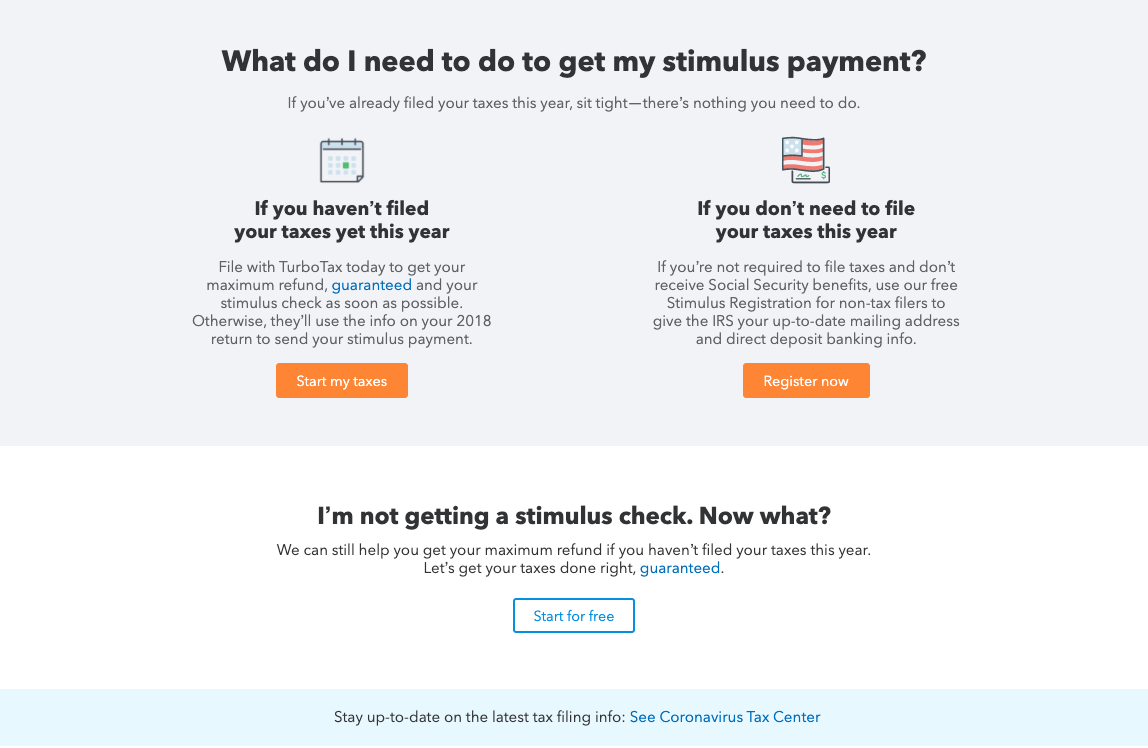

Stimulus Check Registration for the Stimulus Package if you have not filed your taxes for 2018 or 2019. This video is for people who are not receiving socials security benefits and need to file taxes in order to get their stimulus check. This is a convenient way to file your taxes in order to receive your stimulus check. This is from the third stimulus package from the Trump Administration. Please see the link below: https://turbotax.intuit.com/stimulus-check/ Please be sure to check out our videos about CARES Act Unemployment, the Paycheck Protection Program forgivable loan, and the EDL Loan from the Small Business Administration. TSP Financial Group, LLC and affiliates and related parties do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Back to Blog

Back to Blog

Congress likely to send taxpayers $1,200 checks in coronavirus aid. Here's who qualifies...3/26/2020  As Washington lawmakers push through a $2 trillion stimulus bill, many Americans can expect to receive checks of up to $1,200 for individuals and $2,400 for married couples. How much you receive varies based on your marital status and adjusted gross income. Here's who qualifies, and who may be excluded, from the payouts the government plans to send "as rapidly as possible." As Congress pushes through a $2 trillion stimulus bill, some Americans can expect checks from the government to help them cope with the economic devastation stemming from the coronavirus crisis. Those payments are expected to be $1,200 for individuals, or $2,400 for those who are married and file income taxes jointly. It also includes $500 per child. But you have to meet certain qualifications in order to be eligible for the money, based on your adjusted gross income in your latest tax returns. If you earn more than $75,000 as an individual, $112,500 as the head of household or $150,000 if you are married and filing jointly, the amount of those checks starts to get reduced. Checks will be reduced by $5 for every $100 exceeding those thresholds. It completely phases out at $99,000 in income for individuals, $146,500 for head of household filers with one child and $198,000 for joint filers with no children. However, you are still eligible for a check if you have no income or if you rely solely on non-taxable government benefit programs like Supplemental Security Income benefits, or SSI, from Social Security. You also must have a valid Social Security number in order to receive the funds. If you didn't yet file a 2019 return, the government will use your 2018 information if it has it. It also may use a 2019 Social Security benefit statement, or Form SSA-1099, or the Social Security Equivalent Benefit Statement, or Form RRB-1099. Some individuals are specifically excluded from receiving payments. That includes nonresident aliens, individuals whose deductions can go to another taxpayer, and estates or trusts. The legislation calls for sending out the payments "as rapidly as possible." Eligible individuals will receive the funds electronically if they previously authorized refunds to be delivered to them that way. Otherwise, they will be sent out via postal mail. Congress' coronavirus relief bill would also significantly expand unemployment benefits for Americans who lose their jobs due to the country's recent economic contagion. Self-employed workers, those seeking part-time work, and workers who quit their job or can't reach their place of work as a result of COVID-19 are among those eligible for benefits. This is a developing story. Please check back for updates.

Back to Blog

(Bloomberg) -- The coronavirus outbreak is turning one luxury treat reserved for special occasions into a meal bargain hunters can afford.

U.S. lobster prices have plummeted to the lowest in at least four years after the spread of the virus halted charter flights to Asia at a time when sales usually boom for Chinese New Year celebrations. The fallout has left thousands of pounds of unsold lobster flooding North American markets and squeezing U.S. businesses that were already hurting from lost sales due to China’s tariffs from its trade war with Washington. “This is like a fatal blow,” said Stephanie Nadeau, owner of Arundel, Maine-based The Lobster Co., which saw orders to Hong Kong shrivel from about 1,000 boxes a week to a total of 120 boxes -- each carrying 33 pounds -- since late January. “I’m about to lay off most of my employees.” The U.S. used to be the main supplier of live lobster to China as exporters tapped into surging demand from the Asian nation’s growing middle class. Buyers turned to relatively cheaper supply from Canada after Beijing placed retaliatory tariffs on American crustaceans in 2018. Lobster Flights Canada typically sent about nine charter flights a week, with a total of 1.5 million pounds of the shellfish, from Nova Scotia to South Korea and mainland China for everything from restaurants and markets to business meetings and weddings. But as restrictions were placed on the borders of Asian nations including China to contain the spread of the virus, Canadian product began flooding the U.S. market. That pushed prices lower, said Liz Cuozzo, seafood market reporter at research company Urner Barry, which has been tracking food prices since 1858. Prices for New England halves -- a whole lobster weighing 1.5 pounds -- have tumbled 17% since Jan. 20 and are currently at $8.10, the lowest for the period since at least 2016, she said. They typically rise this time of year as supplies are tighter before the main fishing season begins. Last year, they cost $10.70, with the 10-year-average at $9.85. Demand for live Canadian lobster has dwindled to 5% of normal volumes since the Chinese New Year when restaurants started canceling reservations and people stayed home, said Stewart Lamont, managing director of Tangier Lobster Company in Nova Scotia. Inventory Swells Companies are storing inventory, directing products to other markets in Europe, North America and the Middle East, and sending more lobster tails and frozen lobster to be processed, he said. It’s not just the U.S. and Canada that are affected. Australia counts China as the main destination for its rock lobster exports and its seafood industry will likely see a significant short-term impact, the nation’s agriculture ministry said in a report. New Zealand said it’ll allow a limited release of rock lobster back into the wild after Chinese buyers canceled orders. There’s a risk that other markets may shut down as the virus spreads, and uncertainty swirls over how many smaller merchants or mom-and-pop restaurants in China may be out of business and not return to buy following the outbreak, said Mark Barlow, owner of Island Seafood in Eliot, Maine. The Lobster Co.’s Nadeau saw her inventory lose 40% of its value as shore prices dipped from C$10 ($7.45) to C$6, and was forced to sell 50,000 pounds at a loss. She is laying off eight people from her staff of 14. “My customers got creamed and I got creamed,” she said. --With assistance from Anna Kitanaka. To contact the reporter on this story: Jen Skerritt in Winnipeg at jskerritt1@bloomberg.net To contact the editors responsible for this story: James Attwood at jattwood3@bloomberg.net, Pratish Narayanan, Patrick McKiernan

Back to Blog

Coronavirus Disease 20193/1/2020

|

RSS Feed

RSS Feed

ServicesVenture Capital Major Project Funding

Business Loans Church Loans Affordable Health Insurance Plans Kingdom Partnerships TSP 121 Coaching My Online Digital Empire VIP Ticket Orders

|

Company |

|

“We are a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for us to earn fees by linking to Amazon.com and affiliated sites.”

TSP Financial Group, LLC © COPYRIGHT 2015-2030. ALL RIGHTS RESERVED.

13650 FIDDLESTICKS BLVD. SUITE 202-175, FORT MYERS, FLORIDA 33912

O: 877.528.0702 | F: 239.236.0211 | INFO@TSPFINANCIALGROUP.COM

13650 FIDDLESTICKS BLVD. SUITE 202-175, FORT MYERS, FLORIDA 33912

O: 877.528.0702 | F: 239.236.0211 | INFO@TSPFINANCIALGROUP.COM